Daily Top US Stock Picks — June 9, 2026: CRM & NOW

Software's dead-cat bounce or a genuine rotation back in? Two enterprise AI names beaten down by the 'SaaSpocalypse' have compelling setups heading into CPI week: Salesforce (CRM, ~$183) where Agentforce ARR hit $1.2B (+205% YoY) and the stock trades at 13.5x non-GAAP P/E — roughly half the sector average; and ServiceNow (NOW, ~$114, pre-market +7%) where 22% Q1 revenue growth, a $27.7B backlog, and Jensen Huang's Computex endorsement of software partners are converging at the 200-day MA. Full fundamentals, technicals, risk factors, and 1–3 month strategy for both.

Global Tech & Growth Research | Equity Research — Issue #8

Macro and market sentiment

Monday's session opens on firmer footing after Friday's chip-led recovery. The S&P 500 closed June 8 at 7,405.73 (+0.30%) and the Nasdaq at 25,929.66 (+0.86%), snapping a three-session losing streak as Micron surged 9% and Nvidia added 2% on the back of a new SK Hynix AI memory partnership.1 Overnight, S&P 500 E-Mini futures rose a further +0.71% and Nasdaq 100 futures +1.40%, with a softening VIX (down ~13% to ~18.80 from Friday's >22 spike) providing additional lift.2

The week's central event is May CPI (Wednesday) and PPI (Thursday). Market participants currently price a 72% probability of at least one Fed rate hike in 2026 following the blowout May NFP print (+172K vs. 80K consensus).2 A soft CPI would materially reset that pricing. Oracle reports Q4 FY2026 earnings Wednesday evening — a near-term AI cloud read-through for the sector. The FOMC meets June 16–17 with an expected hold.

The session's most notable sector rotation: software stocks are leading pre-market gains after Nvidia CEO Jensen Huang told the Computex 2026 conference in Taipei Monday morning that AI agents will create the "largest opportunity for partner companies" — and named enterprise software platforms as primary beneficiaries.3 ServiceNow opened +7% in premarket on that catalyst; Salesforce is following the sector higher. Both are the picks for today.

콘텐츠 카드를 불러오는 중…

| Metric | As of June 8 close / June 9 pre-market |

|---|---|

| S&P 500 | 7,405.73 (+0.30% June 8) |

| Nasdaq Composite | 25,929.66 (+0.86% June 8) |

| VIX | ~18.80 (down ~13% from prior day) |

| 10Y Treasury yield | ~4.55% |

| S&P 500 E-Mini futures (June 9 AM) | +0.71% |

| Nasdaq 100 futures (June 9 AM) | +1.40% |

| Fed hike probability (≥1 hike 2026) | ~72% |

Pick 1: Salesforce (CRM) — AI execution discount

Current price: ~$183 (52-week range: $163.52 – $276.80)

YTD performance: approximately –28%

Investment horizon: 1–3 months

Investment thesis

Salesforce's fiscal Q1 2027 earnings (reported May 27) handed bears a clear problem: the stock fell 28% before the print, and the print came in better across every measurable line — revenue, EPS, Agentforce ARR, token volume — yet the stock barely moved. That disconnect between execution quality and price is the setup.

Agentforce ARR crossed $1 billion this quarter — reaching $1.2B, up 205% YoY — ahead of the internal timeline that management had guided.45 Including the broader Agentforce + Data Cloud 360 + Informatica platform, Salesforce now carries $3.4 billion in AI and data ARR — a number the bears largely ignore when citing only the narrow $1.2B Agentforce figure. Token consumption rose 152% sequentially to 286 trillion, with 3.8 billion agentic work units delivered in the quarter (+111% QoQ).4

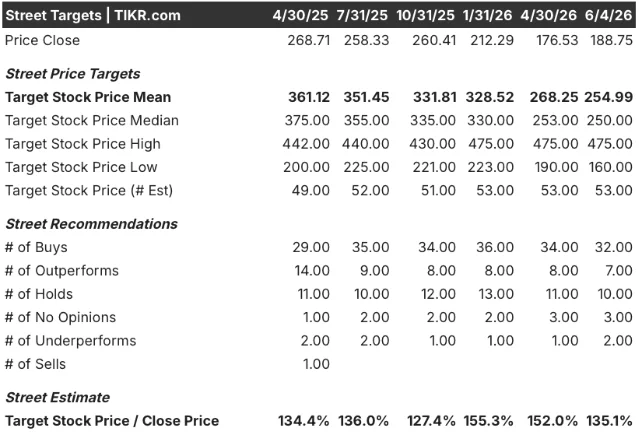

The bear case — per BofA analyst Tal Liani's May 18 Underperform at $160 — rests on three concerns: limited new logo additions, capped upsell potential against a saturated Fortune 500 base, and Agentforce's monetization being "underwhelming."6 Liani values the company at 9x 2027 EV/FCF, implying a transition to a mature cash generator. That is a plausible scenario. The counterpoint is that Salesforce returned $14 billion to shareholders in FY2026 alone (99% of free cash flow), carries $72.4 billion in remaining performance obligations, and trades at 13.5x non-GAAP forward P/E — roughly half the enterprise software sector average.6

The institutional read is split but notable: Starboard Value exited in Q1 2026; Michael Burry disclosed a new long position in April, characterizing the sell-off as fear-driven.6 32 of 51 covering analysts rate it Buy or Outperform, with a consensus target of $260.85.7 Wall Street's average has not moved down to validate the BofA thesis.

Fundamental snapshot

| Metric | Q1 FY2027 (quarter ended Apr 30, 2026) |

|---|---|

| Revenue | $11.13B (+13% YoY, beat est. $11.05B) |

| Non-GAAP EPS | $3.88 (+24% beat vs. $3.12 consensus) |

| Subscription & support revenue | +14% YoY |

| Agentforce ARR | $1.2B (+205% YoY) |

| Combined AI + Data ARR | ~$3.4B |

| Agentic token volume | 286T (+152% QoQ) |

| Remaining performance obligations | $72.4B |

| Diluted share count | –10% YoY (ASR buyback impact) |

| FY2027 revenue guide | $45.9B–$46.2B (+~10.5%) |

| Non-GAAP operating margin target | 34.3% |

| Non-GAAP forward P/E | ~13.5x |

| 52-week high | $276.80 |

| YTD change | –~28% |

Technical picture

CRM's RSI stands at approximately 51 — neutral, not overbought.8 The stock has been consolidating between $163 (52-week low) and $210 (50-day range upper band) since the late-March software sector de-rating. Post-earnings, the stock stabilized in the $183–$192 band. The MACD was negative going into earnings, turned positive on the Q1 beat, and has been flat since — consistent with accumulation rather than trend breakout. Key upside levels: $192 (50-day range midpoint), $210 (50-day upper), $230 (gap fill from the March breakdown).

Risk factors

- Q2 guide miss: Management guided Q2 FY2027 revenue to $11.27B–$11.35B, below the $11.36B consensus.4 Organic subscription growth (stripping Informatica) was 7.7% at constant currency — well below the headline. If Agentforce fails to reaccelerate organic growth in H2 FY2027 as management promises, the stock will re-rate lower.

- AI cannibalization: BofA's seat-license disruption thesis has real structural merit. If Agentforce agents displace seat licenses faster than they generate net new ARR, revenue growth compresses without a corresponding P/E re-rating.

- Macro sensitivity: CRM is a long-duration asset priced on terminal value. A hot CPI Wednesday keeping the 10Y above 4.5% pressures the multiple.

Investment strategy (1–3 months)

The entry window ($180–$190) is defensible with a 13.5x non-GAAP P/E floor and $3.4B combined AI ARR that is compounding faster than consensus gives credit for. The ORCL earnings Wednesday (a read-through on enterprise cloud demand) and the June 11 CPI are the near-term binary events. A soft CPI or a strong ORCL cloud number would catalyze a move toward $210.

Entry: $180–$192 | Target: $230–$250 (3 months, consensus mean $261) | Stop/reassess: Close below $165 (52-week low) or Q2 FY2027 organic subscription growth decelerates below 6%.

Pick 2: ServiceNow (NOW) — agentic AI's governance layer

Current price: ~$114 (pre-market bid ~$122 on June 9)

YTD performance: approximately –19%

Investment horizon: 1–3 months

Investment thesis

ServiceNow has the cleanest enterprise AI compound growth story in software right now, and the stock has spent six months trading as if the opposite were true.

The "SaaSpocalypse" trade — the February selloff triggered by fears that AI agents would eliminate SaaS seat licensing — hit ServiceNow harder than most, pulling the stock 47% from its $208.94 one-year high to an intra-day low below $100. The irony is that ServiceNow's AI Control Tower is precisely the platform enterprises need to govern the explosion of AI agents that allegedly threatened the company. Bank of America analyst Tal Liani — the same analyst who slapped Salesforce with Underperform — reinstated NOW with a Buy rating, calling the Control Tower "mission-critical."3

Q1 2026 confirmed the numbers. Total revenue hit $3.77B, up 22% YoY. Subscription revenue also grew 22%. Net income was $469M on a 76.6% gross margin.9 Backlog reached $27.7B (+25%), and the company raised its full-year 2026 revenue guide to $15.7B (+21% YoY).10 Most importantly, management lifted its AI ARR target from $1B to $1.5B after $750M was already booked by quarter end — a pace that makes the $1.5B target look conservative.

The Nvidia angle is new and significant. At Computex 2026, Huang said AI agents would be "the largest opportunity" for software partners — naming ServiceNow's ecosystem specifically.3 The NVDA–NOW partnership announced March 5 to build enterprise AI agents is now getting valued by the market. The software ETF IGV rallied 21% in May — its best month since October 2001 — as the same capital that rotated out in February began rotating back in.

콘텐츠 카드를 불러오는 중…

Against that backdrop, NOW at ~$114 (or ~$122 pre-market) is still 45% below its 52-week high and 6% below its 200-day moving average of $121.71. Earnings were solid, the AI narrative has been validated by Huang's comments, and a fresh institutional Buy is on the board.

Fundamental snapshot

| Metric | Q1 2026 |

|---|---|

| Total revenue | $3.77B (+22% YoY) |

| Subscription revenue | +22% YoY |

| Net income | $469M |

| Gross margin | 76.6% |

| Backlog | $27.7B (+25%) |

| AI ARR target raised | $1B → $1.5B |

| AI ARR booked by Q1 end | $750M |

| FY2026 revenue guide | $15.7B (+21% YoY) |

| 50-day MA | ~$98 |

| 200-day MA | $121.71 |

| 52-week high | $208.94 |

| YTD change | –~19% |

| Consensus analyst target | $141.85 (avg), $236 (high) |

Technical picture

NOW's RSI was deeply oversold below 32 at the May lows, before the 14% single-day reversal on May 29 (following Dell's blowout earnings).11 RSI has since recovered to approximately 54.5 — neutral, with momentum to the upside.12 The 50-day MA (~$98) is now well below the current price, meaning the stock has recovered nearly 20% from lows and broken above its short-term average. The make-or-break level is the 200-day MA at $121.71: a weekly close above that level would shift the technical signal from recovery to trend reversal.

The pre-market +7% today (June 9) on Huang's Computex remarks puts the stock approaching that 200-day line at market open. Volume confirmation on the breakout will determine whether this holds.

Risk factors

- Earnings risk (next quarter): ServiceNow's Q1 beat masked a 75-basis-point headwind from delayed Middle East deals.13 If deal slippage continues into Q2, the strong backlog number may not convert to recognized revenue on pace.

- Multiple compression: NOW still trades at a premium to enterprise software peers (roughly 21x forward P/E per 247WallSt data). In a rising rate environment, that valuation remains exposed if the CPI print Wednesday comes in hot.

- $120 support as key inflection: If the premarket gains fade and NOW closes below $120, it re-enters the consolidation range. A close below $110 would negate the recovery thesis.

- Competitive pressure from Microsoft and SAP: Microsoft Copilot Studio and SAP's Business AI suite target overlapping enterprise workflow automation budgets.

Investment strategy (1–3 months)

The structural setup is favorable: 22% revenue growth, $27.7B backlog, institutional re-rating, and a Nvidia halo from Computex. The risk is the 200-day MA at $121.71 acting as ceiling rather than floor. A 1–2 day wait for the CPI print Wednesday is a viable way to size into the position with more certainty on rates — if CPI is soft, NOW has clear runway to $140+.

Entry: $115–$125 (scale in, with more weight toward the lower end) | Target: $140–$160 (3 months; consensus $141.85, bull case $236) | Stop/reassess: Weekly close below $105 (structural support per Chartmill), or Q2 2026 revenue guidance reduced below 20% YoY growth.

Comparative snapshot

| CRM | NOW | |

|---|---|---|

| Price (June 8 close) | ~$183 | ~$114 |

| Pre-market June 9 | ~$185 | ~$122 (+7%) |

| YTD change | –~28% | –~19% |

| Revenue growth (latest Q) | +13% YoY | +22% YoY |

| Gross margin | ~78% (non-GAAP) | 76.6% |

| AI ARR / AI metric | $1B+ Agentforce ARR | $750M booked, $1.5B target |

| Forward P/E (non-GAAP) | ~13.5x | ~21x |

| 52-week high | $276.80 | $208.94 |

| Discount from 52W high | –34% | –45% |

| Consensus target | $260.85 | $141.85 |

| Upside to consensus | +43% | +24% |

| Key near-term catalyst | ORCL read-through + CPI | 200-day MA break + CPI |

| Bear case | BofA $160 (seat displacement) | Rate sensitivity, deal slippage |

Key catalysts and calendar (June 9–17)

| Date | Event | Relevance |

|---|---|---|

| June 9 | Computex 2026 / Nvidia partner remarks | NOW pre-market catalyst; positive for software sector |

| June 10 | Oracle Q4 FY2026 earnings | Enterprise AI cloud demand read-through for CRM |

| June 11 | May CPI | Single most important data point for both picks |

| June 12 | May PPI | Follow-through on inflation trajectory |

| June 16–17 | FOMC meeting | Expected hold; tone on future hikes matters for multiples |

Bottom line: CRM is the cheaper, higher-FCF-yield option with a sharper value floor and a contrarian catalyst (Agentforce ARR compounding that consensus underprice). NOW is the higher-growth story at a higher multiple, with a technical breakout setup and a momentum tailwind from Jensen Huang's software endorsement. Both are pricing in a level of AI disruption pessimism that Q1 results do not justify. CPI Wednesday is the shared binary — position accordingly.

Analyst note: All prices are last known at time of writing (June 9, 2026, pre-market). This report is for informational purposes only and does not constitute investment advice. Past performance does not guarantee future results.

참고 출처

- 1Yahoo Finance: Stock market today June 8 2026

- 2Schwab Market Update June 9 2026

- 3Stocktwits: Why Is NOW Stock Surging In Premarket

- 4TIKR: Is Salesforce stock undervalued in 2026

- 5Stoxcraft: Salesforce just beat Q1 FY2027

- 6AOL/TheStreet: BofA resets Salesforce stock price target

- 7MarketBeat: Salesforce CRM

- 8Chartmill CRM technical analysis

- 9Motley Fool: Is Salesforce or ServiceNow a better stock

- 10Seeking Alpha: May AI kill SaaS but supercharge ServiceNow

- 11AOL/247WallSt: ServiceNow soars 14%

- 12Chartmill NOW technical analysis

- 13TIKR: ServiceNow fell 6% Friday

이 콘텐츠를 둘러싼 관점이나 맥락을 계속 보강해 보세요.